# A tibble: 6 × 6

LotFrontage LotArea MasVnrArea TotalBsmtSF GrLivArea SalePrice

<dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

1 50 8500 0 649 1317 40000

2 65 6040 0 0 1152 82000

3 33 4456 0 736 1452 113000

4 52 6240 0 816 1176 114500

5 110 8472 0 816 816 110000

6 60 7200 0 780 780 124900Model Selection

Regularization Methods

Last week: stepwise selection

We learned how to select a model using stepwise algorithms

these are greedy algorithms

results depend on the order in which variables are selected

variables are either in or out

If we can think out as the estimated coefficient being \(0\), can we smoothly shrink the estimator instead of selecting between a value and \(0\)?

Today: regularization methods

Regularized methods

Can we select and train models at once?

Biased estimators

Dataset

Let’s use part of the Ames Housing dataset to introduce and illustrate regularized methods.

Stepwise Selection

Let’s use the “forward” selection algorithm on this (smaller) training set to select some of the variables to predict SalePrice

Housing_forward_sel <- regsubsets(

x = SalePrice ~ ., nvmax = 19,

data = training_Housing[,c(1:5,20)],

method = "forward",

)

summary(Housing_forward_sel)[[1]] (Intercept) LotFrontage LotArea MasVnrArea TotalBsmtSF GrLivArea

1 TRUE FALSE FALSE FALSE FALSE TRUE

2 TRUE FALSE FALSE FALSE TRUE TRUE

3 TRUE FALSE FALSE TRUE TRUE TRUE

4 TRUE FALSE TRUE TRUE TRUE TRUE

5 TRUE TRUE TRUE TRUE TRUE TRUECoefficients of selected variables

(Intercept) GrLivArea

816.3893 119.0938 (Intercept) TotalBsmtSF GrLivArea

-40522.44180 83.88263 88.12881 The estimated coefficient for TotalBsmtSF “jumps” from 0 to 83.88.

Similarly for other coefficients in other steps.

Can the selection be done more “smoothly”??

Regularization methods!!

Regularization (or penalized or shrinkage) shrink coefficients in a continuous way by adding a penalty to the objective funcion.

Mathematically, instead of minimizing the RSS

\[ \ \min_{\beta_0, \boldsymbol{\beta}} \ \sum_{i=1}^n \left(Y_i - \beta_0 - \boldsymbol{X}_i \boldsymbol{\beta} \right)^2 \]

we minimize the penalized RSS, for example:

\[ \sum_{i=1}^n \left(Y_i - \beta_0 - \boldsymbol{X}_i \boldsymbol{\beta} \right)^2 + \ \overbrace{\lambda \ \sum_{j=1}^p \, \beta_j^2}^{penalty} \ \]

Ridge vs LASSO: penalty

We’ll focus on 2 methods (there are many other penalty functions one can use!)

Ridge uses an \(L_2-\)norm to measure the size of the coefficients \[\lVert \beta \rVert_2^2 = \sum_{j = 1}^{p} \beta_j^2\]

Lasso uses an \(L_1-\)norm to measure the size of the coefficients \[\lVert \beta \rVert_1 = \sum_{j = 1}^{p} |\beta_j|\]

Ridge vs LASSO: objective function

Ridge

\[ \sum_{i=1}^n \left(Y_i - \beta_0 - \boldsymbol{X}_i \boldsymbol{\beta} \right)^2 + \ \overbrace{\lambda \ \sum_{j=1}^p \, \beta_j^2}^{penalty} \ \]

LASSO

\[ \sum_{i=1}^n \left(Y_i - \beta_0 - \boldsymbol{X}_i \boldsymbol{\beta} \right)^2 + \ \overbrace{\lambda \ \sum_{j=1}^p \, |\beta_j|}^{penalty} \ \]

The penalty parameter

Scroll down to see full content

How much to shrink??

\(\lambda\) is called the penalty parameter

If \(\lambda = 0\), the objective function of the shrinkage methods is the same as that of LS!! Same estimators!!

As \(\lambda\) grows, coefficients are shrunk.

- LASSO eventually shrinks them all to zero

- Ridge will never reach a value of zero

The penalty parameter \(\lambda\) can be selected using the data. This process is called “tuning”.

- an option is to select the value that yields the smallest \(\text{MSE}_{\text{test}}\).

- this tuning is done using an internal cross-validation or a validation set so that the model does not use test data

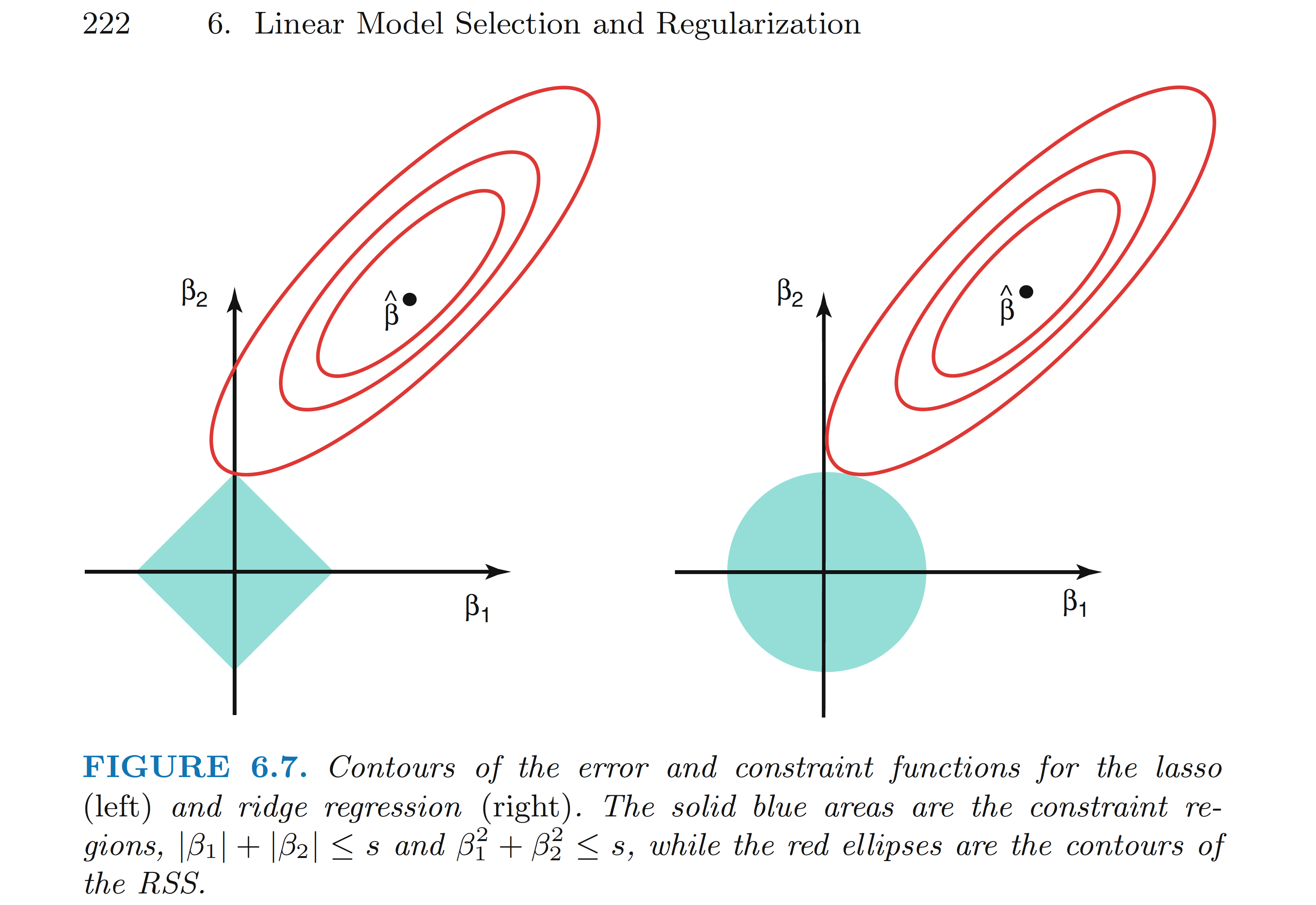

Equivalently, we can think that we impose a bound on the size of the coefficients.

Figure from ISLR book

Ridge

Proposed in 1970 by Hoerl, A.E. and Kennard, R. in

It does not shrink parameters to \(0\), so it does not select variables

It has been proposed as a method to address multicollinearity problems (we’ll skip the math)

LASSO

The least absolute shrinkage and selection operator

Proposed in 1996 by Tibshirani in

it does shrink coefficients to \(0\), thus it can be used to simultaneously select and train (estimate) a model!!

It has been proposed as a method to select strong predictive models

Bias

This “shrinkage” process biases the estimated coefficients!

- we sacrifice bias for a lower variance to potentially gain prediction performance!!

Important: since the method depend on the size of the coefficients, we need to standardize the input variables (default option)

In R

Scroll down to see full content

To build a regularized regression we can use the package glmnet in R. Check this useful vignette

the

glmnet()function requires: a matrix with input variables and a vector of responsesthe argument

alpha = 1corresponds to a LASSO penalty andalpha = 0for a Ridge penalty

There are infinite other options in between known as Elastic Net

glmnet()selects a grid of \(\lambda\) values by default or you can specify oneit is recommended to use given extraction fuctions to obtain the objects, e.g., estimated coefficients

the function

cv.glmnet()can be used to find an “optimal” value of \(\lambda\) by cross-validation

CV creates many test sets from the training set (we’ll see CV later)

- we can visualize how the estimated test MSE changes for different values of \(\lambda\)

Step 1 -3

- create matrices

- set

alpha = 1for LASSO - create a grid of

lambdavalues (try using the default as well)

Housing_X_train <- as.matrix(training_Housing[,-20])

Housing_Y_train <- as.matrix(training_Housing[,20])

Housing_X_test <- as.matrix(testing_Housing[,-20])

Housing_Y_test <- as.matrix(testing_Housing[,20])

Housing_LASSO <- glmnet(

x = Housing_X_train, y = Housing_Y_train,

alpha = 1,

lambda = exp(seq(5, 12, 0.1))

)

Step 4

Scroll down to see full content

- extract estimated coefficients for a given level of regularization

20 x 1 sparse Matrix of class "dgCMatrix"

s=40000

(Intercept) 1.116881e+05

LotFrontage .

LotArea .

MasVnrArea .

TotalBsmtSF 1.447926e+01

GrLivArea 3.126415e+01

BsmtFullBath .

BsmtHalfBath .

FullBath .

HalfBath .

BedroomAbvGr .

KitchenAbvGr .

Fireplaces .

GarageArea 9.785771e+00

WoodDeckSF .

OpenPorchSF .

EnclosedPorch .

ScreenPorch .

PoolArea .

ageSold . Step 5

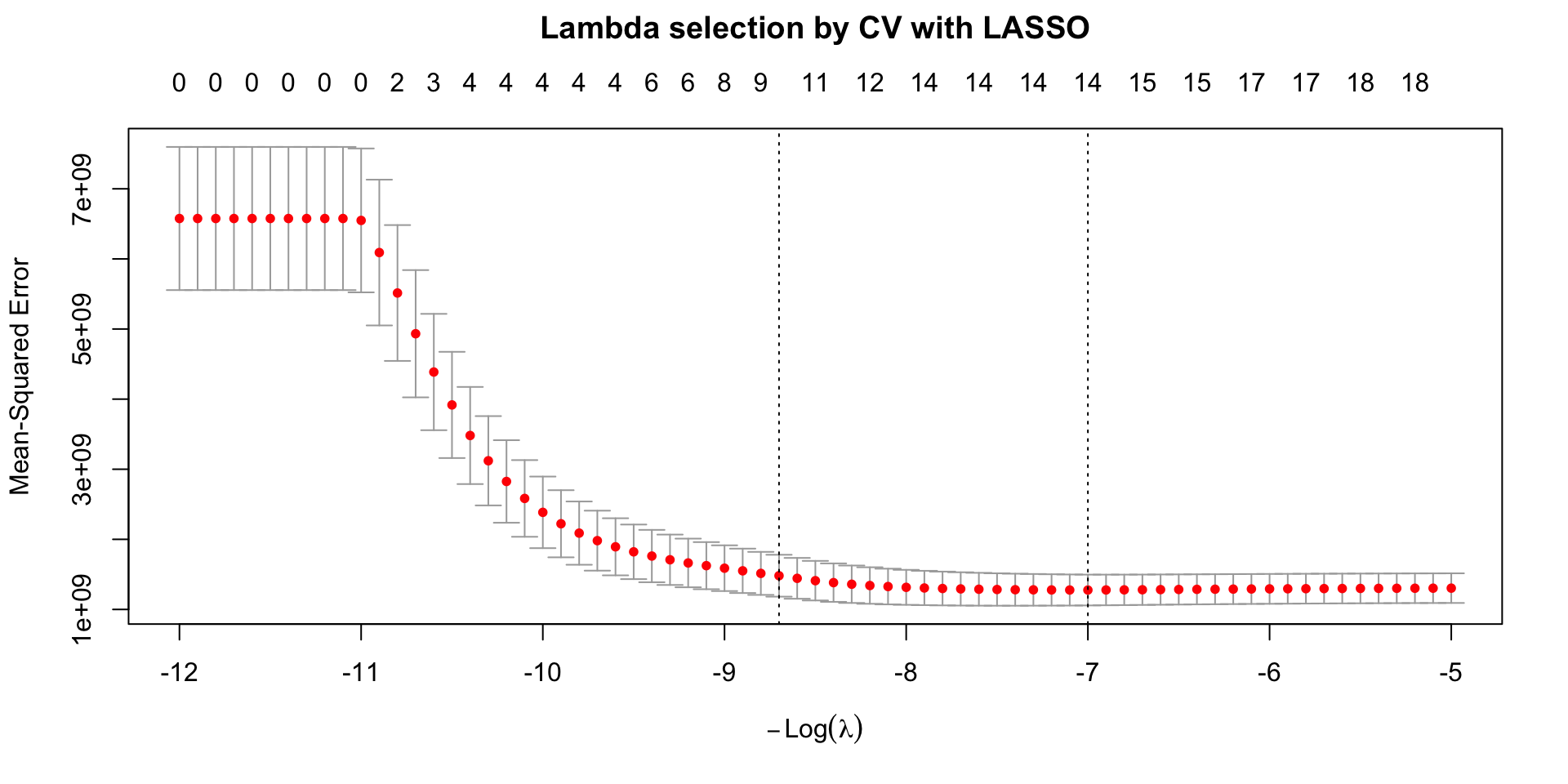

- select the best lambda by CV

Minimizing the MSE

The plot shows the estimated (by CV) test mean squared error (MSE, \(y\)-axis) for a grid of values of \(\lambda\) (\(x\)-axis on the natural log-scale).

the numbers at the top \(x\)-axis indicate the number of inputs whose estimated coefficients are different from zero for different values of \(\lambda\).

the error bars represent the variation across the different test sets of the CV (folds)

Selection of penalty level

The two vertical dotted lines correspond to two values of \(\lambda\):

\(\hat{\lambda}_{\text{min}}\) which provides the minimum MSE in the grid.

\(\hat{\lambda}_{\text{1SE}}\) largest value of lambda such that the corresponding MSE is within 1 standard error of that of the minimum (more penalization at a low cost)

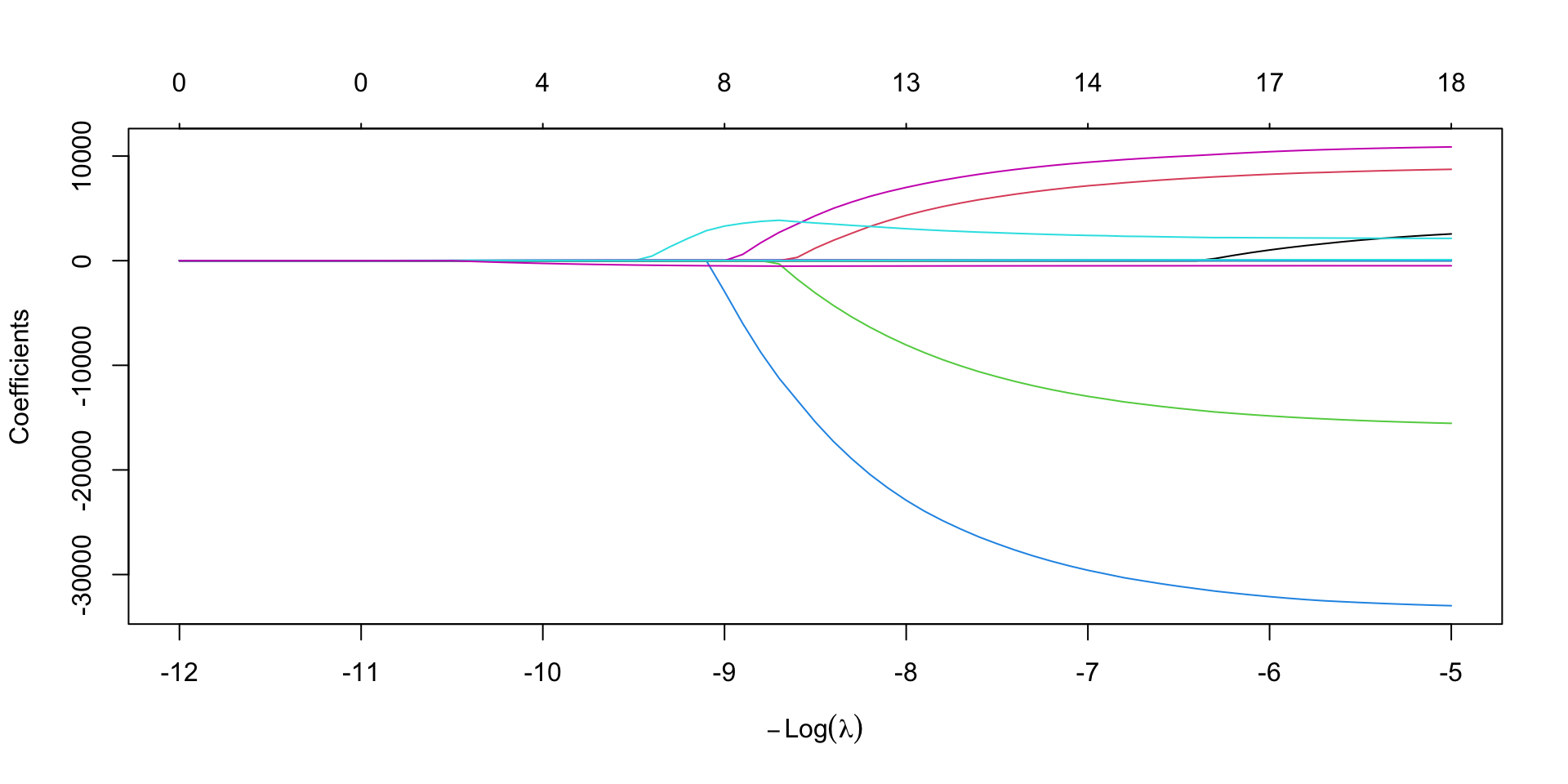

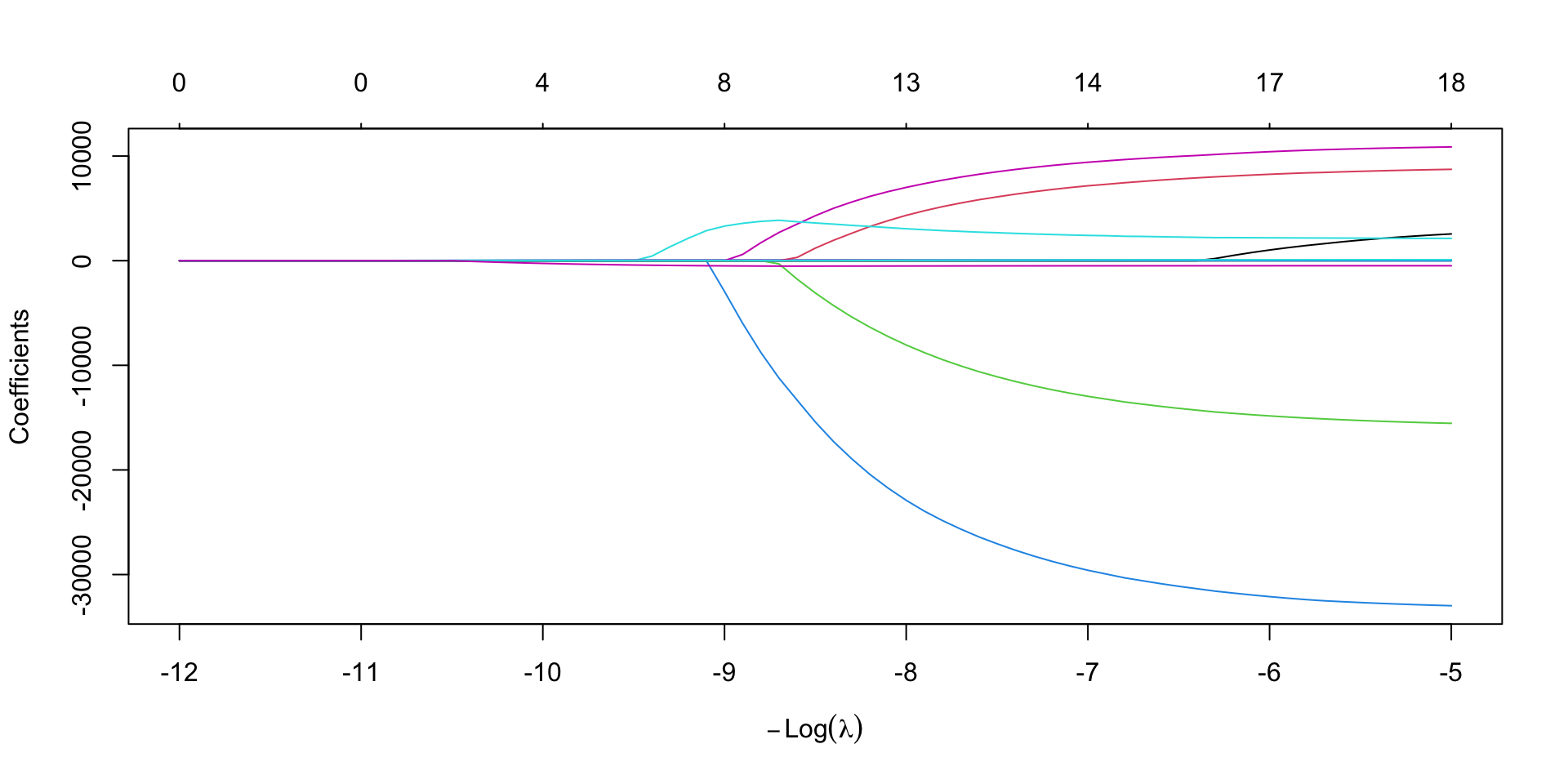

LASSO “smoothly” selects variables and trains the corresponding model for the values of lambda in the grid

Step 5 targeted

5’. extract the estimated coefficients that minimize the CV-test MSE (or the 1SE option).

20 x 1 sparse Matrix of class "dgCMatrix"

lambda.min

(Intercept) 44109.52081

LotFrontage .

LotArea 1.74035

MasVnrArea 32.59693

TotalBsmtSF 37.95458

GrLivArea 80.90134

BsmtFullBath 9407.91300

BsmtHalfBath .

FullBath 7159.11808

HalfBath .

BedroomAbvGr -12964.72474

KitchenAbvGr -29590.90301

Fireplaces 2414.90241

GarageArea 46.58762

WoodDeckSF 10.59831

OpenPorchSF 20.08263

EnclosedPorch .

ScreenPorch .

PoolArea 73.23908

ageSold -489.95991Prediction

LASSO was proposed as a method to build strong predictive models. Let’s use it to predict SalePrice in the test set.

Housing_test_pred_LASSO_min <-

predict(Housing_cv_LASSO,

newx = Housing_X_test,

s = "lambda.min")

tibble(Housing_Y_test,LASSO_prediction = Housing_test_pred_LASSO_min) %>% head()# A tibble: 6 × 2

Housing_Y_test[,"SalePrice"] LASSO_prediction[,"lambda.min"]

<dbl> <dbl>

1 223500 231772.

2 140000 164854.

3 129900 153479.

4 118000 93876.

5 279500 239443.

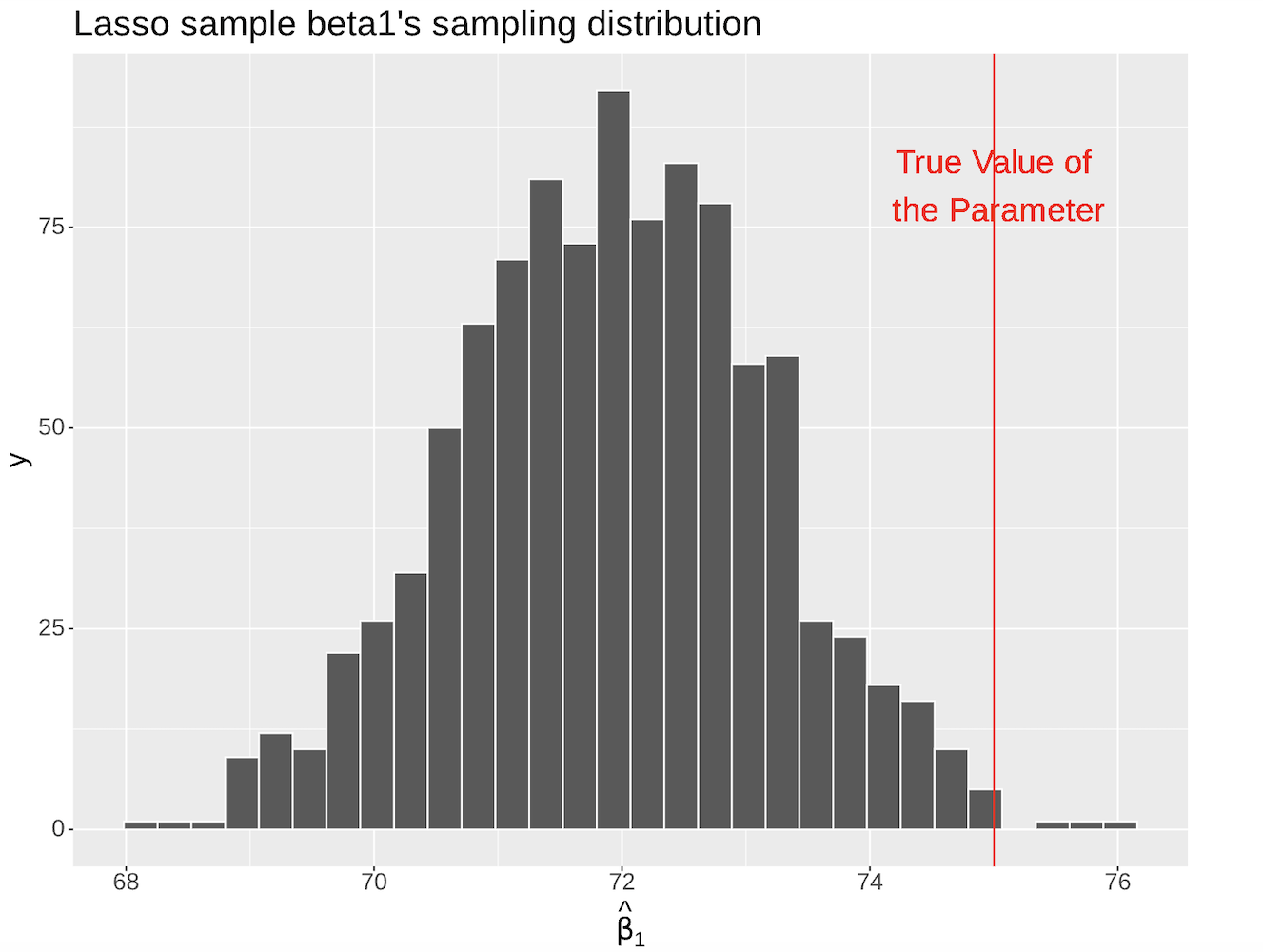

6 132000 98443.Can we use LASSO for inference??

The main drawback of using LASSO for inference is that the estimated coefficients are biased. (in worksheet_08)

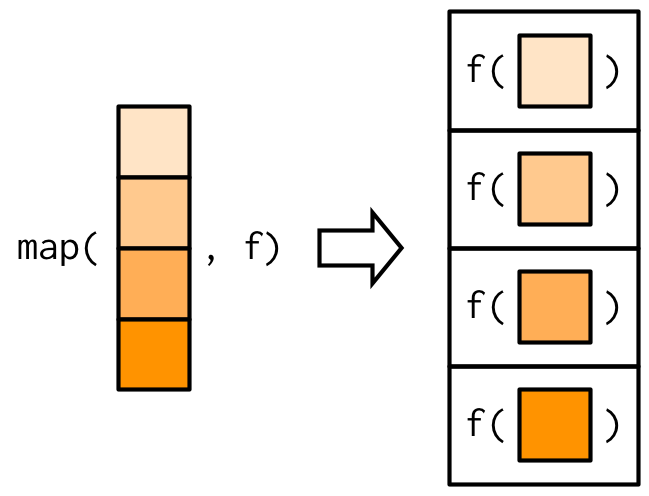

The map function

In the worksheet and tutorial, you’ll simulate data to explore different problems related to model selection.

the function

mapapplies different funtions to a list of datasets (identified by thereplicatevariable)the output of

mapis also a list

Image from Advaced R, by H. Wickham

For example (from your worksheet)

mapis used to fit LS to each dataset using the functionlm(f in the figure)the output is a list containing the elements

replicate,data, andmodels(the fitted models)!!

© 2026 Gabriela Cohen Freue – Material Licensed under CC By-SA 4.0